Financial Education and Starting your Personalized Plan

Everyone deserves to feel confident, capable and in control when it comes to their money. Financial Literacy and Education are a few elements to make that a reality.

Topics you should feel comfortable with include (but not limited to):

- Financial Goals – Click List of potential goals

- Employment Benefits – Download the PayStub Flowchart (attached)

- Budgeting

- Cashflow – Click for Cashflow Checklist

- Saving

- Investments

- Insurance

- Credit

- Loans and Debt – Download the Should I Pay off My Debt Flowchart (attached)

- Taxes

- Banking

- Housing

- Car Buying

- Recognizing Scams and Fraud

Take your finances to the next level with some practical tips and step-by-step guidance. For checklists or Flowcharts for other topics, please email me with your request – hfifield@osaicwealth.com.

If you’re ready to start your Financial Journey, schedule some time with me to help you create your plan and get you on the right track. Click here to complete the Start My Financial Plan checklist

Retirement Strategies for every age

Investing, by nature, involves some uncertainty, and it’s easy to get caught up in day-to-day moves when markets are volatile. Successful investing for retirement is all about thinking long-term.

When you’re in your 20s, retirement might still be decades away. That can make market volatility an investment opportunity.1 There are two related reasons to consider investing more aggressively when you’re young.

First, younger investors may handle market ups and downs easier because they have time before they tap those retirement funds.

Second, with time on your side, you can benefit from the concept of compounding interest, or returns. Let’s say you’re 25 and started saving $5,000 a year in your 401(k). You’ve invested 60% in stocks and 40% in bonds, and your goal is to retire at 65. According to historical averages over the past 30 years, this mix would have earned an annual average return of 8.6%.2 Using this average rate, by the time you’re 65, you would have earned just north of $1.5 million.3

Citations:

1 Morningstar: “The Importance of Staying Invested in Volatile Times” by Daniel Needham, March 16, 2020

2 Disclosure: Historical returns for the period of January 1, 1990 to December 31, 2019, calculated using a hypothetical mix of 60% S&P 500 Index and 40% Bloomberg Barclays US Aggregate Bond Index, rebalanced monthly. Returns generated from Morningstar Direct. Indexes are unmanaged and cannot be invested in directly.

3 Disclosure: Figure generated using “Future Value Calculator” from calculator.net using a 8.6% annual rate, $5,000 for annual contributions, and 40 years of growth.

Question: What is the most important element of investing in the market?

- Contribution frequency and amount?

- Investment vehicle?

- high yield growth potential (with high risk) or

- steady/low yield growth (with low/no risk)

- high yield growth potential (with high risk) or

- Time in the market?

Answer: Time!

Your retirement income planning should start when you first start working as time is the most important component in the savings and investing equation.

You need time to take advantage of compound interest.

Example:

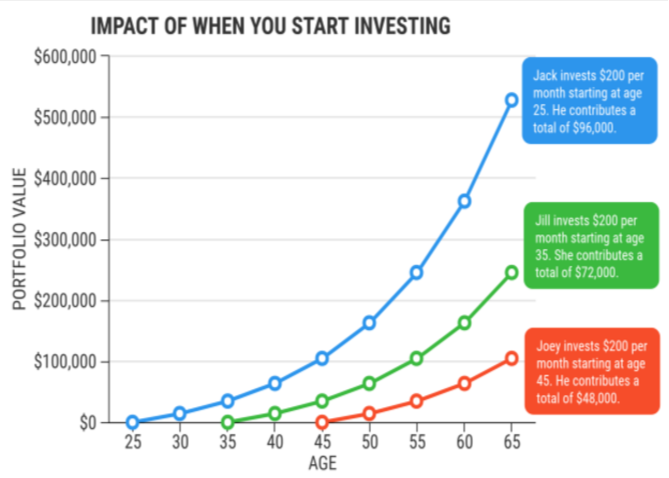

Why Investing Early Is the Key to Financial Success

The stock market is kindest to those who stay faithful to it longest. To see this in action, consider investors Jack, Jill and Joey.

Jack starts investing $200 per month when he's 25. By age 65, his portfolio is worth more than $520,000.

Jill doesn't start investing until age 35. She also contributes $200 per month, but by 65, her portfolio is only worth about $245,000. By waiting 10 years to start, she ends up with less than half of what Jack accumulates.

Joey, the late bloomer, starts investing $200 per month when he's 45, and after 20 years he has only $100,000.

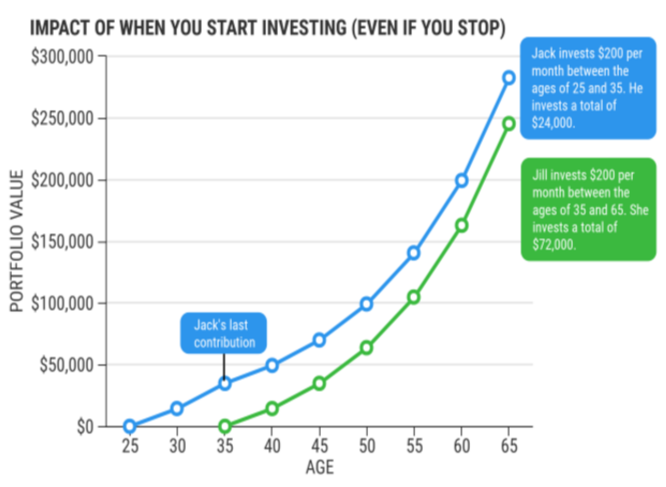

When You Start Investing Matters More Than How Much You Invest

Time invested is so important that Jack can even stop adding to his investments and still have more than Jill at age 65.

If Jack were to contribute $200 per month from age 25 to 35 – contributing only $24,000 over 10 years – his investments would be worth almost $300,000 at age 65.

Jill continually invests $200 per month between ages 35 and 65 but still ends up with only $245,000 at 65. Even though she contributes three times as much as Jack over her lifetime ($72,000), because she missed those first 10 years of investing, Jack amasses more.

The initial consultation provides an overview of financial planning concepts. You will not receive written analysis and/or recommendations.